GBV 2023 Outlook

Surviving is the prerequisite to making it. We are still here in the game, despite all that has happened in 2022, and notwithstanding the damoclean sword of DCG that hangs above the crypto market.

Here, we offer our outlook of the 2023 crypto market.

Layers 1 and 2

From 2020 to 2022 we saw an explosion of layer-1s - many with high FDV and low adoption. As we dive deeper in 2023, the shakeout will continue and out of that comes the continued deflation of these layer-1s. We believe chains that have already acquired a significant user base at the height of the bull market are poised to make a comeback. Devastating as the collapse of FTX was for the Solana ecosystem, the retail baptised into the ecosystem through Solana NFTs and STEPN still carry their wallets and their SOL with them. And as the bull market returns, interest in crypto and the explosion of on-chain activity that threatens to make Ethereum again economically prohibitive to use, will force users and value to overflow into altchains and Layer 2s.

Indeed, we can expect to see the sum of all layer 2 TVL to flip the sum of alt layer-1 TVL in 2023. We anticipate Arbitrum to dominate while Optimism does alright. We think zk(e)vms will all underperform expectations, with starknet underperforming the least since it's most orthogonal to the existing Ethereum dApp ecosystem. We wouldn’t be surprised if Polygon runs into trouble for overspending in the bear market to inorganically acquire partnerships.

We are keeping a keen eye on the Cosmos ecosystem. Though still fiddling with its tokenomics, the potential of the Cosmos SDK to spin up new chains with unique ecosystems has already been proven through the Canto chain - a degen chain with the same technology as EVMOS, except that there is no VC backing, and that all financial primitives accrue value back to the validators.

Though early and barren as of this moment, the quasi-fair launch of the chain, lends the chain ample potential to grow organically to become a new degen playground.

DeFi

DeFi is the chief value proposition of blockchain technology. Blockchain allows trustless ownership of assets without resorting to the courts, and DeFi unlocks the financial potential of these assets.

DeFi will remain the chief and mainstream crypto native use case.

Despite all the technological strides of the 2020-2022 bullrun, the most important problem in DeFi still has not yet been solved. The problem of Liquidity Rental, whose list of solutions include Pool 2 and Olympus’ (3,3) meme, remains unsolved. The holy grail of a capital efficient, decentralised, and scalable stablecoin, remains elusive.

The collapse of FTX, though devastating, has only further proven the case for DeFi.

Having said that, we think there are good reasons to be cautious with exposure to decentralised perp exchanges. Although it is true that decentralised perp exchanges like GNS and GMX are superior to some of the traditional finances liquidity solutions like CFDs in terms of slippage and UX, and that the explosive success of Robinhood and indeed Crypto in general since 2020 is unequivocal proof that gamified finance satisfies a deep market demand, the oversaturated mindshare of these protocols, coupled with suppressed trading volumes now, have created an environment where pools can get rekt with less dollar value. Furthermore, thanks precisely to the success and the TVL of these protocols, these protocols would be the most popular targets of hacks in the crypto space. These are highly complicated DeFi protocols with extremely labyrinthian codebases. It is only within expectations that bugs keep emerging. Forks are more prone to these issues as their team’s understanding of the codebase might not be as thorough.

Over 2023, we expect a further pruning of what is useful and what is not useful in the DeFi space. The primitives with consistent usage will be the winners.

We are confident that the old protocols like Uniswap, Aave, Compound, and Curve will remain strong. Although new protocols with better designs will emerge to challenge these incumbents, (e.g. Euler), we think success is going to be limited.

Furthermore, as we go deeper into the bear market, TVL will continue to dwindle, and along with that is the amount of trading fees chargeable by protocols. Revenue generation becomes more and more pressing an issue.

A convergent evolution of business models in DeFi appearing before us. Instead of deriving revenue directly by charging users of the protocol a fee, protocols like AAVE and Curve are launching stablecoins in which interest payments are all accrued to the protocol itself. The stablecoin itself serves as the tool for liquidity provision, thereby alleviating the protocol pressure for incentivizing liquidity. Liquidity becomes fully owned and controlled by the protocol. The inevitable final component, would be the introduction of Algorithmic Market Operation (AMO) modules, where the mother protocol directly mints its own stablecoin into other pools or protocols to earn fees, thus transforming the protocol from a liquidity renter to a liquidity provider.

We are also cognizant of the latest developments in the DeFi options space. However, we must say we are at best cautiously optimistic about these highly complicated structured product vaults. Although the technology is very exciting, adoption amongst cryptonative folks is likely going to be limited by the sheer complexity of these products. Widespread adoption like the kind that allowed Axie and STEPN’s explosive growth are probably out of reach for these protocols, if the market population remains to be retail and degen folks. The catalyst for the growth of these protocols would be the arrival of institutions, who need sophisticated tools to hedge risk, and who are capable of understanding and using these products for profit.

“The first XYZ protocol on ABC chain” is not going to cut it anymore. New solutions and new designs will have to emerge. Interesting candidates include clearinghouses for Decentralised Perp Exchanges, and hybrid designs between AMM and orderbooks.

There are very few reasons to believe ponzis will not make a comeback in the next bull market. It has practically been a law of crypto that folks who made it this cycle must retire lest they ruin themselves with excessive degeneracy that ends up on the wrong side. And as they retire, they retire their knowledge, and experience with them. It has not been widely noted but trying to understand crypto history through twitter is a nigh impossible task. Tweets get deleted, accounts get shadow banned, and OGs stop accepting follows into their private accounts - and not to mention the rumours and articles and essays that dive deep into the chronology of events. There is therefore every reason to believe that new arrivals at the crypto scene will make mistakes that have already been made, under the promises of obscene wealth that we have already encountered.

NFT

NFTs are things in the digital space. Where there are people with money, there will always be people who want to buy stuff.

We are confident that NFTs will prove itself to be a superior form of digital goods. The free2play gaming market has generated 23B in 2021 alone, however, those goods are not freely tradable and remain locked on AWS servers. Furthermore, those virtual goods have a huge bottleneck of only being able to be purchased mostly through in-app purchases through apple or android (with 30% fees and 500$ limit per purchase!). NFTs on open blockchain networks offer interoperability and permissionless composability, allowing them to strictly dominate garden-walled digital goods that live on AWS. It would simply be untenable to sell digital goods that aren’t NFTs in the future. NFTs will be widely adopted, buyers will start demanding NFTs as they're superior in terms of utility, tradability, interoperability, and security.

It is a good heuristic to mentally compartmentalise NFTs into three categories: PFP NFTs (Punks, BAYC, Pudgy Penguins, Azuki, etc), Art (Autoglyphs, Chrome Squiggles, etc), and Gaming NFTs (Realms, Digidaigaku, etc).

NFTs remain the primary object of flexing in the crypto community. Memetic desires coalesce into price floors for NFTs. Gaming NFTs (skins and in-game weaponry) require their own gaming community to accrue flex value. Given blockchain games are still at their infancy, we think art and vanilla PFPs are better poised to satisfy the flex market - and this market demands Veblen goods. If it ain’t expensive, it conveyeth no social status.

Putting that argument into practice yields a bullish thesis for the major PFPs that emerged this cycle. In particular, we believe Punks will do extremely well in the long run. As the NFT market inevitably grows, Punk’s status as the first ever NFT PFP collection on Ethereum to ever exist will cement its veblen goods status and its community of prominent influencer holders such as Jake Logan Paul lent good popular cultural support to the collection. Furthermore, unlike Bored Apes where the collection of associated NFTs keeps expanding via mints like Mutant Apes, Otherside and MDVMM, which in very cynical eyes be seen as nothing more than just inflation, Punks has no inflation of any sort and no difficult to deliver promises of game development.

We think the NFTFi sector faces multiple challenges for it to gestate its own summer. The prerequisite for an NFTFi summer is composable NFTFi protocols stacking on top of one another. However, an NFT without an associated income stream has limited financialisation potential. Consider the NFT-Fi (protocol) and Metastreet vertical. A NFT is collateralised for loan origination, and these loans are then bundled together for mass purchases and trading. The question here is how to scale this? There are only so many blue-chip pfp NFTs good enough to serve as collateral for loan origination.

For NFTFi to really boom, we believe the size of collateralisable NFTs have to be multiples of the current market size and the NFTs themselves need to offer utility and cashflow. The most promising kinds of NFTs that can fulfil this role are likely gaming NFTs and music NFTs. However, the nascency of the sector gives one reason to believe that there’s still a long way to go.

GameFi

We have yet to really see blockchain games that are not DeFi with extra steps. Blockchain gaming will need to solve problems of scalability and propose token models beyond the dual model for it to escape hyperinflationary deaths. Although there are interesting developments such as bottom-up games such as Lords and Treasure DAO, highly celebrated projects such as Axies and STEPN, sustainability and playability remains elusive.

Sustainability remains elusive because we still have not yet figured out how to go beyond the dual token model and P2E. We have not yet gone beyond P2E because we GameFi projects need to subsidize players to make up for their lack of playability. Though Avalanche subnets and Cosmos-SDK app chains promises to deliver the speed and throughput necessary to breed playability, we have yet to see something concrete.

We are keeping a keen eye on Gabriel Leydon’s Digidaigaku. Gabriel Leydon is the CEO of limitbreak, the company behind Digidaigaku. Leydon was the co-founder and former CEO of Machine Zone, the company behind huge games such as Mobile Strike and Game of War, which amassed more than $4.5 billion in revenues from 2014 to 2018. What intrigues us about Digidaigaku is Gabriel Leydon’s strong understanding in free-to play gaming gives us hope that there might be a breakthrough in gaming economics.

Instead of selling NFTs or using fungible tokens to pay people to play the game, a gaming studio should give out NFTs, which serves as gaming assets, for free. Players then build out and upgrade these assets as they continue to play the game. The gaming studio makes money through selling upgrades, accessories, and enforceable resale royalties. Enforceable royalties are particularly important. In late 2022, as marketplaces moved to zero-royalty and royalty-optional trades in a battle for liquidity, this created an environment where creators are simply not incentivized to stay.

The creator-token-contracts released by Limitbreak, which provides a framework for holders to stake their NFT to wrap it with a new token that enables more specific programmable properties, opens up a backwards-compatible, opt-in system that allows developers to upgrade their collections without sacrificing immutability. This enables creators to have control over things like resale royalties, rentability, staking rewards, and minimum resale floor prices.

We think this innovation is not to be ignored. Right now, marketplaces wield control the flow of ETH. With programmable NFT properties, the flow of ETH is reintroduced back into the hands of creators. This allows creators to control the financial properties of an NFT, thereby opening up a whole new programmable possibility space for incentives, royalties, and game mechanics.

DeSo

Web2 is becoming increasingly unusable. Google search results are overrun with ads and content farm articles. The tiktokification of everything from Youtube to Instagram threatens to poison the masses with cheap dopamine. Recognition of the toxicity and unusability of web2 is on track to become not just VC consensus but public consensus in 2023. The kind of content and community degradation forcing folks to add “reddit” or “stackexchange” in their google queries, the user exhaustion from deplatforming and censorship, and black swan collapses like Yahoo’s acquisition and decimation of Tumblr, are all potential catalysts for Decentralised Social Media (DeSo) to take flight. Indeed post-Elon, Twitter has already seen its wave of exodus to alternative social media like Mastodon.

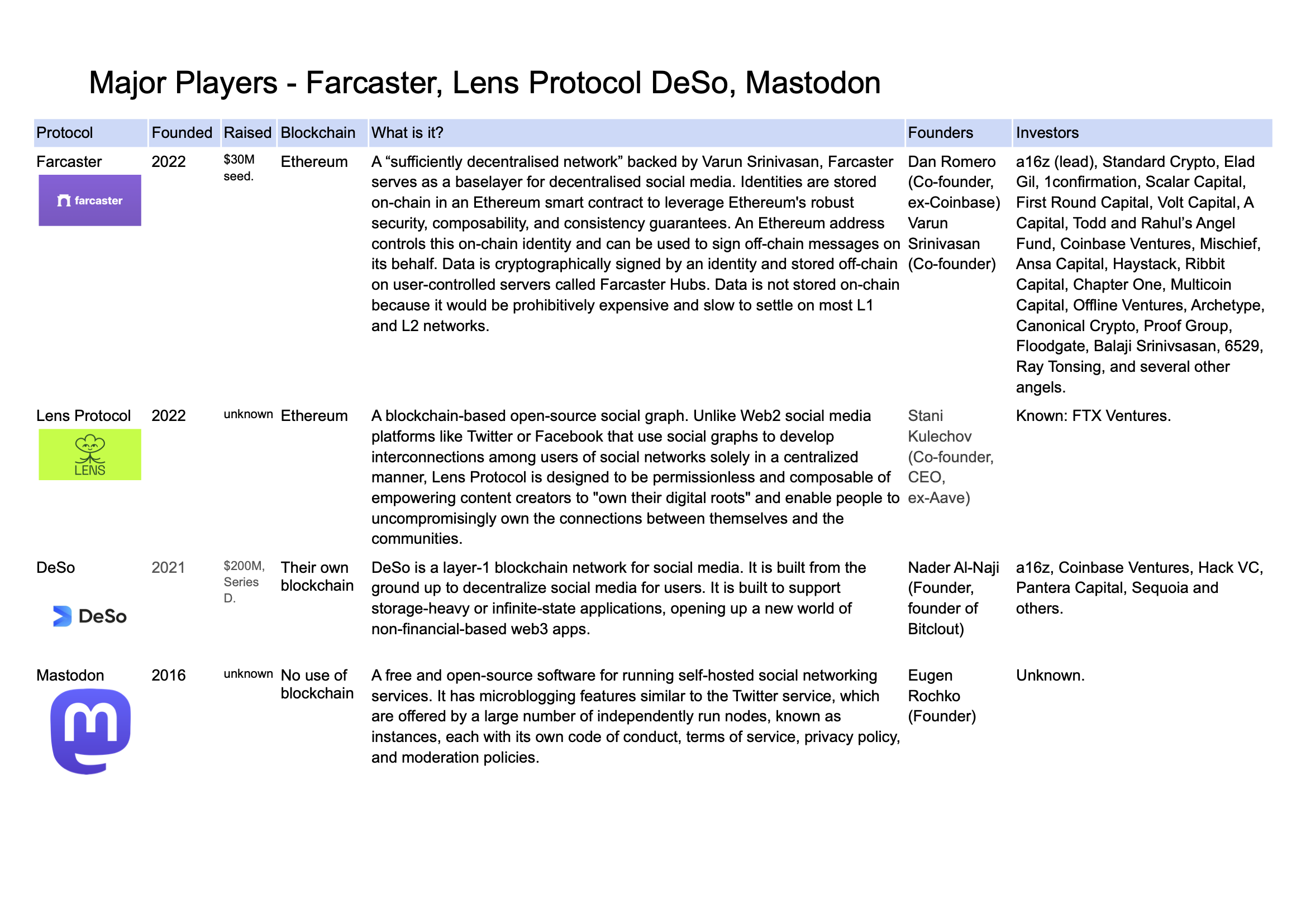

Amongst the competing web3 projects out there, we keep a close eye on Farcaster and Lens protocol. Farcaster’s minimalist approach of storing data on-chain and its permissionlessness allows for different developers to query data from Farcaster and build different, custimized apps atop the Farcaster data layer. Lens in comparison is more complicated as the protocol is not just a data layer but a social graph, complete with asset types that track the relationship between followers and the followed. We believe the Farcaster’s more minimalist and cautious approach is more likely to prove wise in the longer run as fewer things, and therefore fewer bugs and debt, are hardcoded in the outset. Having said that, the potential for Lens for becoming a social credit rating protocol for undercollateralised lending on AAVE is extremely interesting.

The space is still in its very early days, with adoption minimal and UX leaving much to be desired. We anticipate more waves of #TwitterMigration over 2023, with users active in adult content production and far-left and far-right political communities leading the exodus. Mass migration is going to be long and meandering, as folks have every reason to not give up the networks, the clout, the social “credit” they have built on web2 social media. However, once they have moved over, users will become hooked to the convenience that comes from DeSo protocols allowing multiple protocols to access to one base social profile. Fragmented social clout and social credit will be a thing of the past.

However, we note that the true test of whether a web3 protocol is truly decentralised is whether it can become part of the “darknet” infrastructure, in which content moderation is added on the level of centralized frontends, thereby allowing users to access the “dark” part through decentralized infrastructure. Otherwise it’s just web 2 social media all over again.

Other undercurrents - VC landscape, dev influx from FAANG, Hong Kong

We expect many VCs forced into redemption. Refunds requested en masse and SAFTs on fire-sale like in '19. Plenty of projects burn through their entire runway, others claiming fallout from FTX. VC fundraises will collapse, and many funds will close as they find themselves sitting on illiquid garbage. There is opportunity amidst this calamity.

Bear markets are for building. Going forward, it is going to be more and more difficult to run a crypto fund with no engineering arm. It is not just code literacy - it is also engineering capability and capacity that is going to be required in this space. Funds that make it in both monetary terms and influence terms are going to be those who build as much as they could analyze.

Going into 2023, we expect not only a continued flushing out of degen crypto funds, but also an escalation of building competitiveness. As on-chain activity dwindles, searchers and MEV wizards find themselves joining projects, thereby raising the dev space competition. Mass layoffs at FAANG also threaten to raise the bar higher. One only needs to be reminded that FTX’s whole stack was built by one ex-Google engineer alone.

Regulations will continue to march against crypto in 2023, along with the advent of the dreaded CBDC. More centralized exchange will be under investigation, and the icky dealings that they’ve been hiding in their underbellies will all be exposed. We do not believe the dominance of CBDCs is a forgone conclusion. We think in most open economies, CBDCs will have to face the market just like any state-led economic action.

We are bullish on Hong Kong’s remergence as a crypto center, for its accommodating regulatory regime, and the influx of Chinese money as they rotate from US assets.

Concluding Remarks

The 2023 outlook is ripe with potential. A potential rebound from the 2022 bear market, the new developments and applications of Layer 1s and Layer 2s, the advances in DeFi technology - all converge to form a promising and exciting year ahead in the crypto markets.